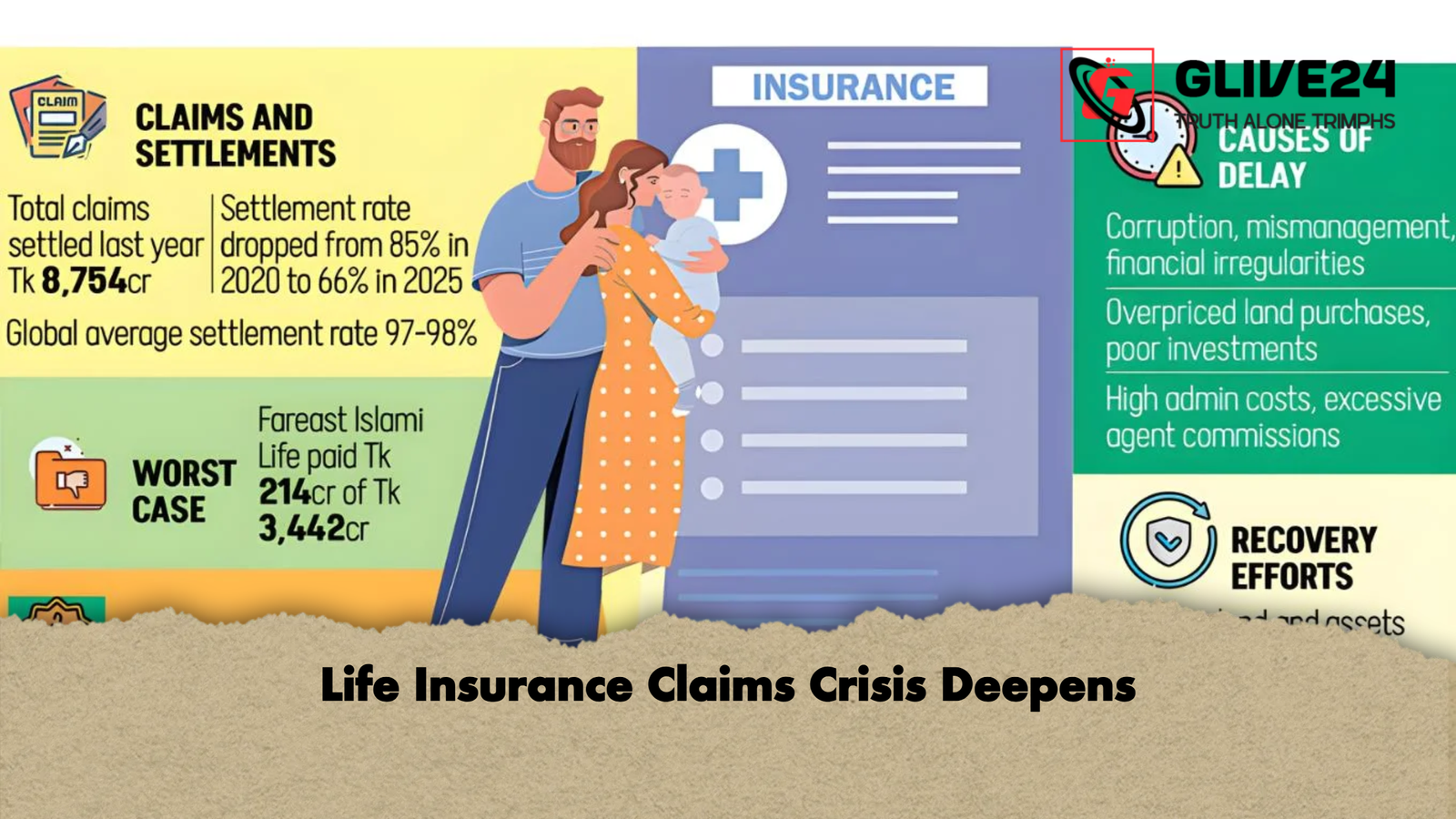

A prolonged financial strain combined with persistent management weaknesses in Bangladesh’s life insurance sector has led to a severe backlog in the settlement of policyholder claims. According to recent figures, around 1.2 million insurance customers are currently awaiting payments, while the total value of unsettled claims has surged to approximately Tk 4,403 crore.

One such policyholder, Monjur Rahman, purchased a life insurance policy in 2012 in pursuit of financial security for his family. Upon maturity in 2022, his entitlement amounted to Tk 1,119,000. Despite submitting all required documentation, he is yet to receive his dues. He further reports that even requests for partial withdrawal during a period of urgent medical need within his family were declined, leaving him under significant financial distress.

Under existing regulations, insurance companies are required to settle claims within 90 days of receiving complete documentation. However, in practice, a substantial number of insurers have failed to comply with this legal obligation, contributing to growing public frustration and eroding trust in the sector.

Table of Contents

Data from the Insurance Development and Regulatory Authority indicates a sharp deterioration in claim settlement performance over recent years. In 2023, approximately 1 million policyholders were awaiting payments totalling around Tk 3,050 crore. By 2025, both figures had risen significantly to 1.2 million claimants and Tk 4,403 crore respectively.

During the same period, the overall claim settlement ratio dropped to 66.06 per cent, a steep decline from 85 per cent in 2020. This contrasts sharply with international benchmarks, where average settlement ratios typically stand at 97–98 per cent in many countries, including major regional economies.

The severity of the crisis varies widely across insurers. While a few institutions have fully met their obligations, several others are struggling with extremely low settlement ratios and large outstanding liabilities.

| Insurance Company | Total Claims (Tk crore) | Paid (Tk crore) | Settlement Rate | Policyholders Affected |

|---|---|---|---|---|

| Fareast Islami Life | 3,442 | 214 | 6% | 5.66 lakh |

| Padma Islami Life | Limited data | Low | 4% | Significant |

| Progressive Life | Limited data | Low | 21% | Significant |

| Golden Life | Limited data | Low | 11% | Significant |

| Sunflower Life | Limited data | Low | 5.5% | Significant |

| Bayra Life | Limited data | Low | 1.6% | Significant |

| Akij Takafol Life | Fully settled | Full | 100% | None |

| Alpha Islami Life | Fully settled | Full | 100% | None |

| Life Insurance Corporation | Fully settled | Full | 100% | None |

| Mercantile Islami Life | Fully settled | Full | 100% | None |

Investigations by regulatory authorities and oversight bodies have pointed to a range of systemic issues aggravating the crisis. These include allegations of fund misappropriation, excessive administrative expenditure, weak investment strategies, and poor asset management.

In several instances, companies are reported to have overvalued property acquisitions and relied heavily on bank borrowing to finance operational gaps, further weakening their liquidity position. Despite the appointment of administrators and periodic restructuring of boards by the regulator, meaningful improvements have remained limited in many cases.

According to a professor from the Department of Banking and Insurance at the University of Dhaka, the crisis is rooted in years of weak investment performance and declining income streams within several insurers. He further suggests that in some cases, claims are being deliberately delayed despite the availability of funds.

Industry specialists argue that without decisive reforms—such as merging financially weak companies, enforcing stricter regulatory oversight, and introducing compulsory health insurance—the sector is unlikely to recover its stability or restore public confidence.

Overall, Bangladesh’s life insurance sector is facing a deepening structural crisis driven by governance failures, financial mismanagement, and inadequate regulatory enforcement. As a result, public confidence continues to erode, while hundreds of thousands of policyholders remain deprived of their rightful entitlements for extended periods

> Extortion Demand Preceded Chattogram Office Attack

> US Weapons Stockpiles Strained by Iran Campaign

> Police Arrest 117,000 in Nationwide 72-Day Crackdown

> Marital Dispute Exposes Buried Murder in Khulna

> Dengue Claims Two More Lives as 327 Hospitalised

> Bangladesh Flood Death Toll Reaches 54 with Thousands Stranded

> Viral Search Links Argentina To ‘Thieves’ Tag

> Twelve Injured in Indian Wedding Brawl Over Mutton Menu Change

> Wife Arrested After Severing Sleeping Husband’s Genitals

> Iran launches new strikes against Kurdish groups in Iraq

> Two Arrested With Tapentadol

> Club Goal Rankings in World Cup History

> Footballer’s Family Missing After Venezuela Quake

> The Psychology and Philosophy of Unwarranted Defamation

> Content maker Al Amin burnt while filming taken to Dhaka

> Simrin Lubaba Begins New Life After Marriage Shift

সম্পাদক ও প্রকাশক: এ বি এম জাকিরুল হক টিটন

যোগাযোগের ঠিকানাঃ পশ্চিম কাফরুল, বেগম রোকেয়া সরণি, ঢাকা

© Copyright 2026 Khaborwala। All Rights Reserved

Comments