Khabor Wala Desk

Published: 6th April 2026, 10:16 AM

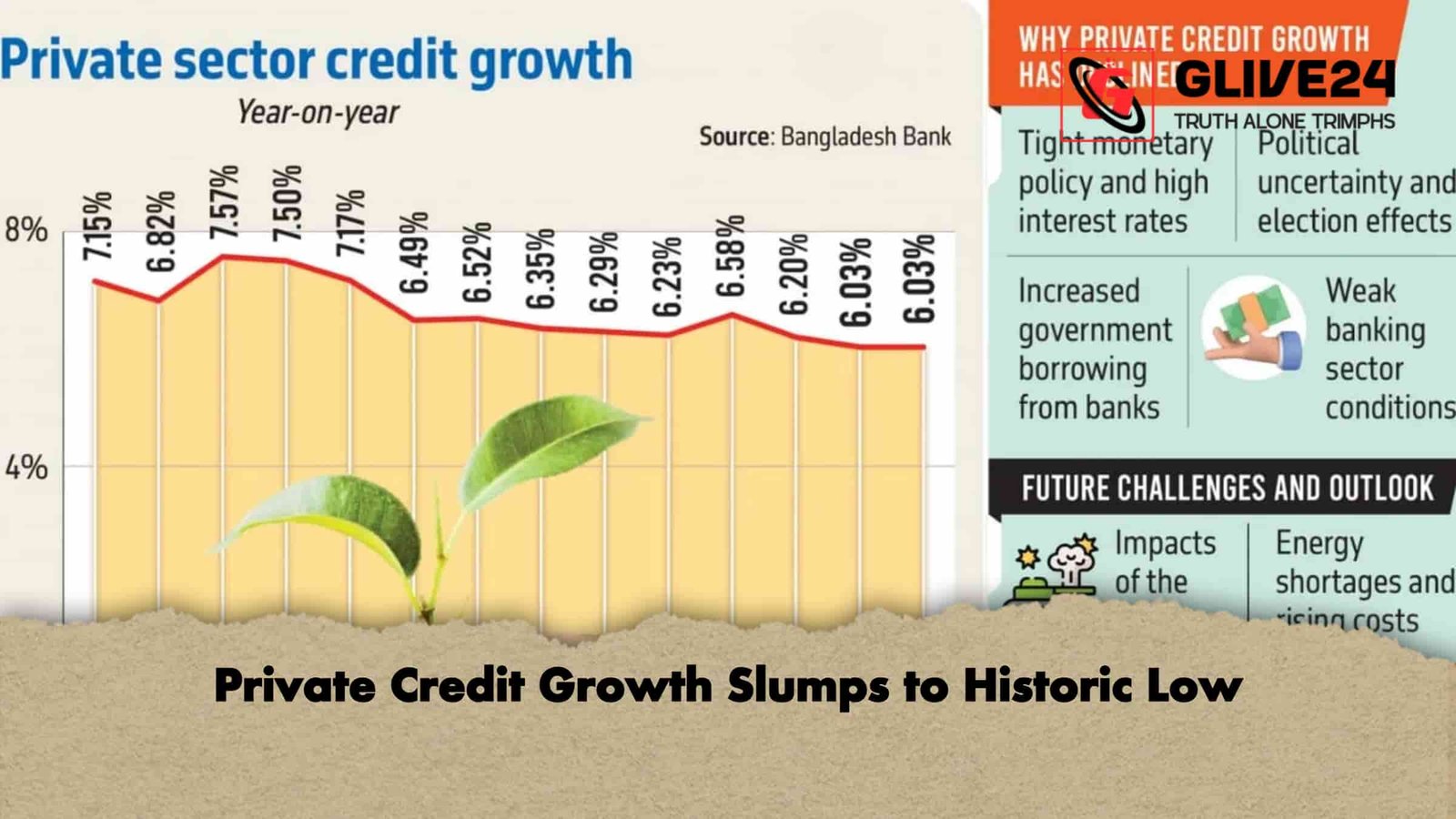

Bangladesh’s private sector credit growth fell to a record low of 6.03 per cent in February, highlighting the continued strain on lending amid political uncertainty and persistently high interest rates. Experts warn that, with the ongoing Iran war creating additional geopolitical risk, a near-term recovery in credit growth is unlikely.

Data from Bangladesh Bank shows that private credit growth has been declining steadily since July 2024, when it stood at 10.13 per cent. The decline accelerated following the political transition in August 2024. A brief rise to 6.58 per cent in November 2025 was largely driven by loan restructuring ahead of the 12 February national election, rather than new investment in productive sectors.

| Month | Credit Growth (%) |

|---|---|

| April 2025 | 7.50 |

| May 2025 | 7.17 |

| June 2025 | 6.40 |

| July 2025 | 6.52 |

| August 2025 | 6.35 |

| September 2025 | 6.29 |

| November 2025 | 6.58 |

| December 2025 | 6.10 |

| February 2026 | 6.03 |

In its January–June 2026 monetary policy statement, the central bank cited tight monetary policy, rising government borrowing, and subdued loan demand amid uncertainty over new investment decisions as key factors behind the slowdown.

Sohail RK Hussain, Managing Director of Bank Asia PLC, told The Business Standard: “Following the February election, the government prioritised private sector growth. Yet the Iran war has created fresh uncertainty. Even if the conflict ends now, credit growth is unlikely to recover in the near term.”

He added that energy costs remain a major hurdle: “High fuel import prices increase production costs and could prompt further interest rate hikes. Combined with rising dollar exchange rates and weak export demand, the coming months will be particularly challenging for businesses.”

Governor Md Mostaqur Rahman, newly appointed to Bangladesh Bank, indicated that the central bank intends to provide policy support to revive lending. Measures include a gradual reduction in lending rates and the reopening of dormant factories to stimulate investment. However, policy implementation has been delayed by ongoing geopolitical and domestic pressures.

Other pressures on banks include rising non-performing loans, which reached Tk5.57 lakh crore by December 2025, and heavy government borrowing—net credit to the government hit Tk98,000 crore, or 94.73 per cent of the revised annual target, by 19 March 2026. High lending rates of around 13.5 per cent continue to limit borrowing, particularly among small and medium enterprises.

The cumulative impact of these factors is evident across the economy: slower industrial expansion, underutilised factories, weak consumer demand, and stagnating private sector employment. Analysts caution that without improvements in energy supply and infrastructure, private sector credit growth is likely to remain subdued for months.

Comments