Khabor Wala Desk

Published: 8th March 2026, 7:20 AM

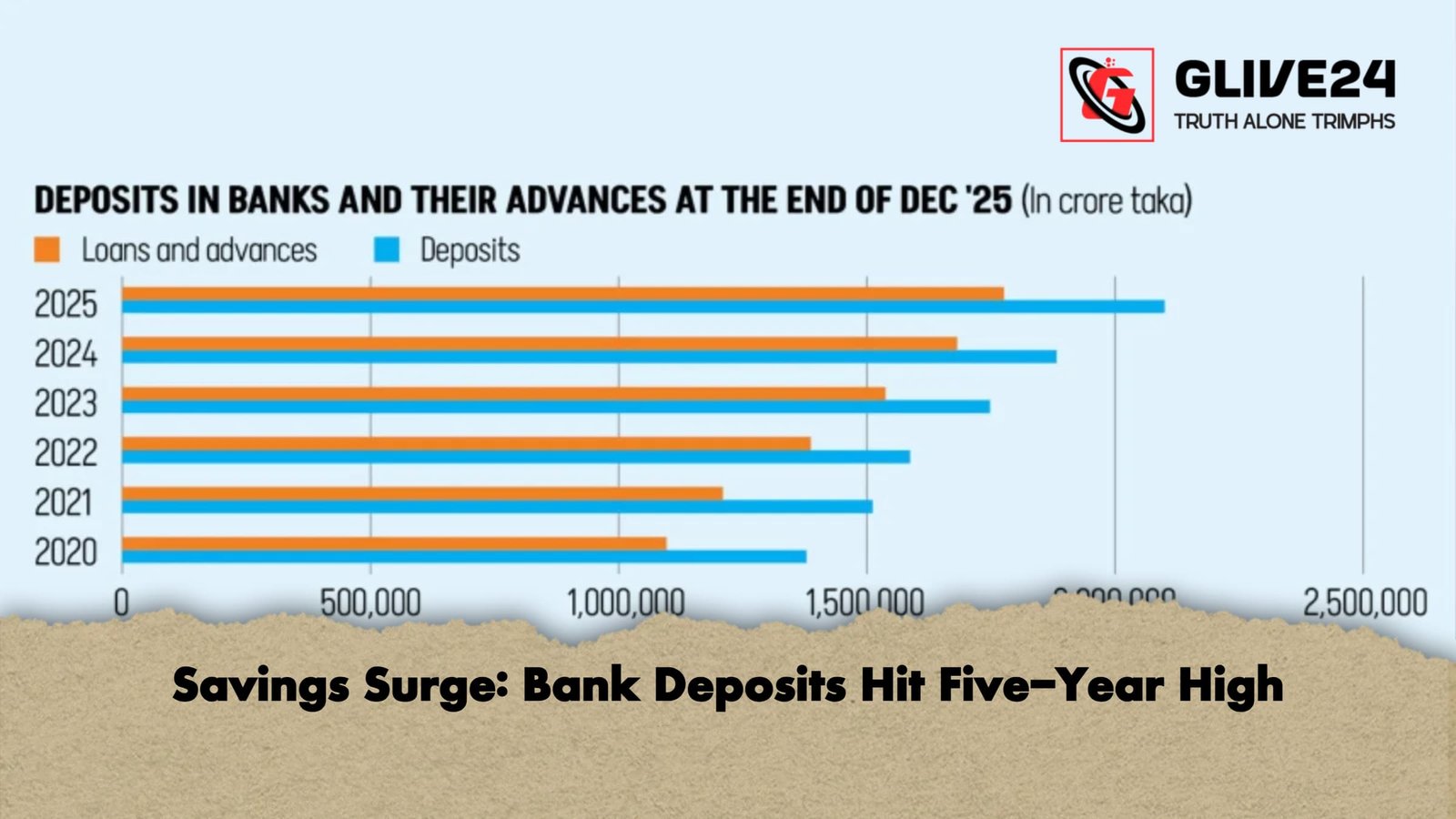

The Bangladeshi banking sector has achieved a significant milestone, with deposit growth reaching a five-year peak at the end of December 2025. This surge is widely attributed to a steady restoration of public confidence in the financial system. According to the latest quarterly statistics from Bangladesh Bank (BB), total savings in the country’s 61 scheduled banks have crossed the historic 21 lakh crore BDT mark.

Table of Contents

The year-on-year growth rate for deposits was recorded at 11.51%, a substantial leap that saw the total figure eclipse the 20 lakh crore BDT threshold for the first time. This recovery follows a turbulent 2024, during which the sector grappled with a severe liquidity crisis and a lack of trust amongst savers. At that time, several institutions faced difficulties returning funds to depositors on demand, necessitating significant capital injections from the central bank.

Industry experts believe the current trend suggests a shift in public sentiment. Md Mahiul Islam, Deputy Managing Director at BRAC Bank, noted, “It appears that people’s confidence in banks is gradually being restored.” However, he cautioned that this windfall is not evenly distributed, with the majority of the new capital flowing into a select group of seven to eight high-performing banks.

The data reveals that private sector banks, including Shariah-compliant Islamic institutions, remain the dominant force in the market, holding nearly 70% of total deposits.

| Bank Category | Deposit Market Share (%) |

| Private Banks (inc. Islamic Banks) | 69.52% |

| State-Owned Commercial Banks | Significant Minority |

| Foreign Banks | Remaining Percentage |

In a striking contrast to the influx of savings, lending activities witnessed their slowest growth in 2025. Total loans and advances rose by only 5.6%, reaching 17.77 lakh crore BDT. This disparity is driven by two main factors:

Rising Interest Rates: High borrowing costs have muted investment demand from the private sector.

Lending Caution: Banks have adopted a defensive stance, tightening credit criteria to avoid the further accumulation of non-performing loans (NPLs).

The Bangladesh Bank Quarterly report suggests that the easing of inflationary pressures has discouraged “dissaving” (spending from savings), encouraging households and businesses to move assets back into the formal banking sector. Furthermore, recent political developments have fostered a more stable environment, enhancing the public’s propensity to trust institutional finance.

While the surplus of deposits provides banks with a strong liquidity cushion, the challenge for 2026 will be translating these savings into productive credit to stimulate national economic growth.

Comments