Aggressive credit expansion by private commercial banks is heightening systemic risk within the national banking sector, according to a recent analytical report issued by the central bank. The assessment identifies three converging pressure points: lending beyond regulatory ceilings, a sustained rise in non-performing loans, and a marked slowdown in deposit growth. Together, these dynamics are straining liquidity conditions and amplifying vulnerabilities, particularly among private and Shariah-compliant institutions.

Under prevailing prudential regulations, conventional banks are permitted to extend loans up to 83 per cent of their total deposits. The remaining 13 per cent must be maintained as mandatory reserves with the central bank to safeguard depositors’ interests. Islamic banks operate under a distinct framework: they are required to maintain a 9.5 per cent reserve, enabling them to invest up to 90.5 per cent of deposits. In addition, all banks must hold supplementary cash balances to meet daily settlement and payment obligations.

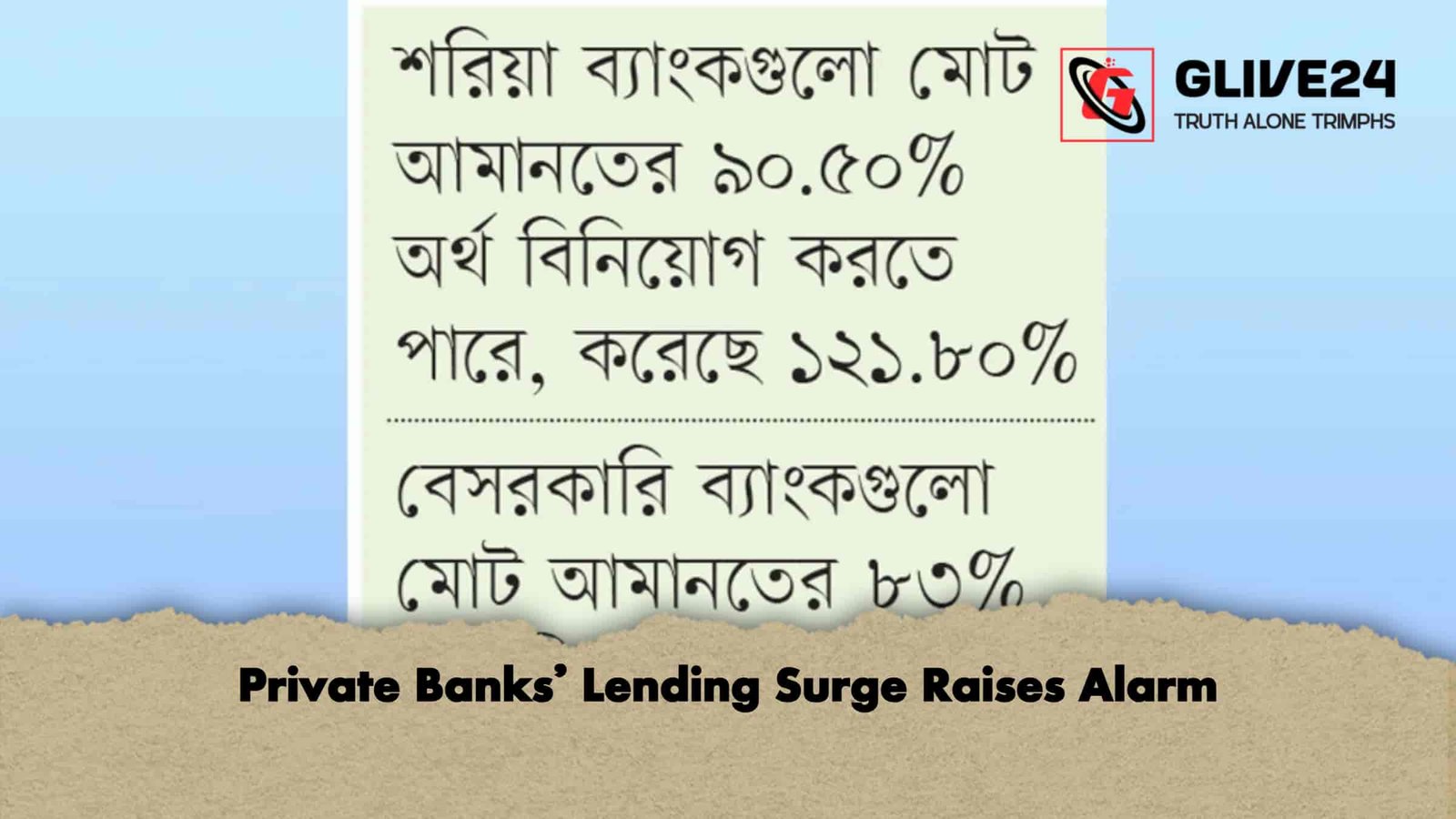

However, the report reveals that a significant number of private and Islamic banks have exceeded these thresholds. On average, private commercial banks have lent 94.10 per cent of their deposits—11.10 percentage points above the permitted ceiling. The position of Islamic banks is even more acute: their investment-to-deposit ratio has reached 121.80 per cent, exceeding the regulatory cap by 31.30 percentage points. Such overextension has reportedly been financed through interbank borrowing and instruments raised in the money market, thereby increasing leverage and refinancing risk.

By contrast, state-owned and foreign commercial banks remain broadly within regulatory bounds, maintaining more conservative liquidity positions.

Comparative Loan and Investment Ratios

| Bank Category | Loan/Investment-to-Deposit Ratio (%) | Regulatory Limit (%) | Deviation (%) |

|---|---|---|---|

| Private Commercial Banks | 94.10 | 83.00 | +11.10 |

| Islamic Banks | 121.80 | 90.50 | +31.30 |

| State-Owned Commercial Banks | 71.70 | 83.00 | –11.30 |

| Specialised State-Owned Banks | 87.00 | 83.00 | +4.00 |

| Foreign Commercial Banks | 55.30 | 83.00 | –27.70 |

The sector-wide average loan or investment ratio currently stands at 86.90 per cent, already above the standard prudential benchmark for conventional institutions. Economists caution that persistent regulatory breaches by certain banks could destabilise the broader financial architecture. Rising non-performing loans are further constraining cash flows, impairing capital buffers, and eroding depositor confidence.

Analysts emphasise that unchecked credit concentration increases exposure to sectoral shocks, particularly in an environment of slowing deposit mobilisation. When loan growth outpaces deposit inflows, banks become increasingly reliant on wholesale funding sources, which are inherently more volatile and sensitive to market sentiment. This dynamic heightens liquidity risk and can trigger contagion effects during periods of stress.

Financial experts therefore advocate enhanced supervisory scrutiny, stricter enforcement of statutory limits, and the adoption of robust risk-based capital management frameworks. Without timely corrective measures, the continued expansion of credit beyond sustainable thresholds may pose a medium-term threat to macro-financial stability, undermining both depositor protection and overall economic resilience.

Comments